Lesson 18 – Property Reversion: Annuity plus Reversion Method (The Income Approach to Value)

Property Tax Rule 8, previously covered in Lesson 5, “Definition of the Income Approach and Property Tax Rule 8”, states, in subsection (b):

(b) Using the income approach, an appraiser values an income property by computing the present worth of a future income stream. … the income stream is divided into annual segments and the present worth of the total income stream is the algebraic sum (negative items subtracted from positive items) of the present worths of the several segments. In practical application, the stream is usually either (1) divided into longer segments, such as the estimated economic life of the improvements and all time thereafter or the estimated economic life of the improvements and the year in which the improvements are scrapped and the land is sold, …

…. In Lessons 16 and 17 we learned about the horizontally divided income described in subsection (b)(2). In this lesson we will learn about income streams divided vertically – in particular, a level terminal income stream combined with a single income payment sometime in the future – a reversion. You may sometimes hear the level terminal income stream called an annuity income, an annuity cash flow, or an Inwood annuity cash flow.

Notes

- William INWOOD (1771-1843) was an English architect and surveyor; he was the author of the Tables for the Purchasing of Estates, Freehold, Copyhold, or Leasehold, Annuities, Advowsons, &c., a forerunner of compound interest and annuity tables such as the AH 505.

Property Reversion: Annuity Plus Reversion Method

When the income stream is a series of equal, annual, incomes, that terminate in the future, the income stream is constant terminal shaped.

When the income is a single payment some time in the future, the income is a reversion.

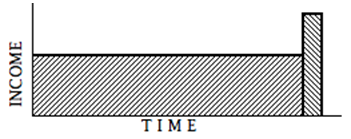

Combine the two, and you have an annuity plus a reversion.

Information needed:

- Net Income Before deducting for recapture and property Taxes [NIBT], or the requisite information to derive NIBT

- Value of Reversion

- Yield rate [Y]

- Effective Tax Rate [ETR]

- Time, such as Remaining Economic Life [REL], until the Reversion

After processing the market income stream to the Net Income Before deducting for recapture and property Taxes level [NIBT], the NIBT is capitalized into the value of the annuity income stream using the Capitalization Rate; V = NIBT ÷ (YO + SFF{@Yo,Ann,REL} + ETR). The Reversion Income (Reversion Value) is the value attributable to the property remaining at the time of the property's reversion – this may be the end of the lease term, or perhaps the end of the property's Remaining Economic Life. Multiplying the Reversion Income by the reversion capitalization factor, which is comprised of the Yo plus the ETR, will give us the Value of the Reversion. Adding the Reversion Value to the Annuity Value will give us the Total Property Value. This can also be expressed in the following format:

EXAMPLE 18-1: Property Reversion Method

Here’s another example. In this scenario the appraiser has determined that the typical investor for this type of property will hold on to the investment for six years. The appraiser concludes that the value to this typical investor is how the market would value the property.

EXAMPLE 18–2: Valuation Using Inwood Annuity plus Reversion Method

Below are the assumptions on which the valuation is to be based. The income to be capitalized is estimated on a market basis and is processed to the level of Net operating Income Before deducting for recapture and ad valorem property Taxes [NIBT]. The reversionary value is estimated based on current value and anticipated inflation. A component for property taxes must be included in the capitalization rate.

Assumptions

Estimated Annual Cash Flows

Present Value Calculations

The capitalization rate is based on the 12% Yield rate plus the Sinking Fund Factor (for the six year Holding Period) plus the 1% Effective Tax Rate.

The Reversion factor is based on the Yield rate plus the Effective Tax Rate (in this case, 12%+1%=13%), for the Holding Period, six years.

PW1{@(Y+ETR),Ann,HP}: 0.480319 PW1{13%,Ann,6yrs}

Summary

The lesson you just read covered the Property Reversion Capitalization, sometimes called the Inwood Annuity plus Reversion Method. The next lesson will address the valuation of personal property, and will use Property Reversion Capitalization.

Note: Before proceeding on to the next lesson, be sure to complete the exercises for this lesson.