Lesson 7 – Cost and Cost Components (Valuation of Personal Property and Fixtures)

Using Assessors' Handbook Section 581 (Equipment Index, Percent Good, and Valuation Factors)

Appraisal Training: Self-Paced Online Learning Session

This lesson discusses cost and cost components. The factors in AH 581 are used by California county assessors to value personal property and fixtures for property tax purposes. The AH 581 factors are applied to equipment and fixture costs to arrive at estimates of market value. Thus it is essential that the costs to which the factors are applied accurately reflect all valid cost components of market values for subsequent lien dates, at the time the equipment on fixtures were purchased or built in order for the resulting value estimate to be a good indicator of value. Businesses in California report their property and corresponding costs to county assessors annually for taxation; reporting is done on property statements.

Open All Close AllDefinitions

This lesson uses several terms that you should be familiar with; below are definitions for certain terms that are used throughout this lesson.

- Business Property Statement: property statements are declarations of assessable property signed under penalty of perjury. They report all taxable property owned, claimed, possessed, controlled, or managed by the person filing it. They are prescribed forms upon which California taxpayers report their business property to county assessors. (Assessable is synonymous with taxable.)

- Direct costs: also referred to as “hard” costs, are expenditures for the labor, materials, and direct factory overhead required to construct the property whether purchased in the form of raw materials or a finished product.

- Indirect costs: also referred to as “soft” costs, include expenditures other than labor and material necessary to make the equipment ready for its intended use.

Components

In valuing personal property and fixtures, it is important to be aware of all cost components. Property Tax Rules 6 and 10 define these components as including labor, material, entrepreneurial services, interest on borrowed or owner-supplied funds, freight or shipping costs, installation costs, sales or use tax, and “other costs typically incurred in bringing the property to a finished state (or to a lesser state if unfinished on the lien date).”

Cost for assessment purposes may be thought of as full economic cost. Full economic cost should include all market costs, both direct and indirect, necessary to purchase or construct equipment and make it ready for its intended use. Costs that add value and are associated with manufacturing equipment and/or making equipment ready for its intended use should be included in the full economic cost. Not all costs add value, for example, relocation costs are not costs contributing to the assessable value of the property. And, not all costs that contribute to value are booked, for example, unpaid but owing sales or use tax.

Typical cost components vary depending upon whether the equipment is purchased or self-constructed. In the case of purchased equipment, typical direct costs are the purchase price including sales tax, freight, trade-in-allowances, and installation costs. In the case of self-constructed equipment, direct costs include such cost components as materials, labor used in construction, direct overhead and sales tax on materials. Refer to Assessors' Handbook Section 504, Assessment of Personal Property and Fixtures, Chapter 4, for additional information on direct and indirect costs.

Property Statements

The valuation of personal property and business fixtures for assessment purposes most often involves the use of a mass appraisal method. The index, percent good, and valuation factors published in AH 581 are intended to be used in mass appraisal to produce market value estimates for property tax purposes in California. The Board prescribes property statement forms for use by the 58 county assessors in California. A property statement, also referred to as a business property statement – the most often used of such statements, is a declaration of assessable business property at a specific location in a county. The property statement is organized to facilitate the use of equipment index, percent good, and valuation factors. Each piece of equipment is not identified and valued separately, but rather, the equipment is valued as a group based on the type of business and the classification of the property. (Note: an exception is Form AH 571-F Agricultural Property Statement, where each item of equipment is listed separately on the form.)

Property statements are organized into two schedules: Schedule A to detail costs for equipment and Schedule B to detail costs for buildings, building improvements, and/or leasehold improvements – bifurcated into structure or fixture items; land improvements; and, land and land development. Costs are reported by year of acquisition and property classification. The classifications of equipment correspond to factors published in AH 581 (i.e., machinery and equipment, personal computers, etc.) With respect to costs reported for machinery and equipment for industry, profession, or trade, an appraiser knows the type of industry or trade that the business is in because it is declared by the filer on the first page of the property statement. Additionally, assessors maintain specific information on property statement filers based on previous filings and audits.

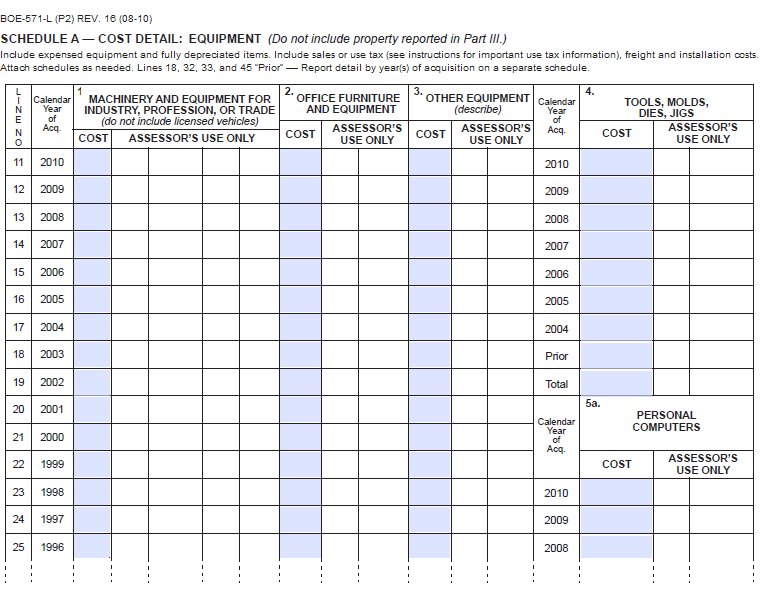

Below is Schedule A of the 2011 Business Property Statement (Form BOE-571-L) to illustrate how costs are reported.

Notice the text directly under the heading Schedule A-Cost Detail: Equipment. It instructs filers to include sales or use tax, freight, and installation costs when reporting costs. It also instructs filers to include expensed equipment and fully depreciated items. Although an item of equipment may be fully depreciated for accounting or income tax purposes, it does not mean it does not have value for property tax purposes. The Instructions for property statements provide further information on reporting costs of equipment – one such direction is to “report full cost: do not deduct investment credits, trade-in allowances or depreciation.”

In valuing assessable business property reported on property statements, assessors use the costs reported – by property classification and year of acquisition – and the factors published in AH 581, to calculate the assessed value.

Lesson Summary

The lesson you just read provides you with information on cost and cost components. It is important to understand what should be included in costs when valuing personal property and fixtures in California, because it impacts the resulting value conclusion. It is, after all, cost to which you apply the index factors, discussed in Lesson 2, or the valuation factors, discussed in Lesson 4. It is also important to understand how property costs, reported to assessors are used in conjunction with index, percent good and valuation factors, to arrive at market value estimates for assessment purposes.

Note: Please proceed to the Summary, for concluding remarks on this learning session.