Lesson 4 – Valuation Factors (Valuation of Personal Property and Fixtures)

Using Assessors' Handbook Section 581 (Equipment Index, Percent Good, and Valuation Factors)

Appraisal Training: Self-Paced Online Learning Session

This lesson discusses valuation factors, one of the types of factor tables that are published in Assessors' Handbook Section 581, Equipment and Fixtures, Index, Percent Good and Valuation Factors (AH 581). The valuation factors are based on market data, for identical or similar equipment and/or fixtures, which compare the used price of such property to its original new price, and produces valuation factors that capture all forms of depreciation and price changes as a result. When reliable, accurate, and representative market data are available, this “market data” method is the preferred method of calculating valuation factors for equipment and fixtures. Analysis of market data and parameters for industry group studies is discussed in AH 581; as well as identification of when studies were conducted. Valuation factors are presented in the following five AH 581 tables:

- Table 7: Non-Production Computer

- Table 8: Semiconductor Manufacturing Equipment & Fixtures

- Table 9: Biopharmaceutical Industry Equipment & Fixtures

- Table 10: Document Processor

- Table 11: Offset Lithographic Printing Presses

Unlike index and percent good factors, valuation factors are not used in combination with other factors to produce an estimate of market value of equipment and/or fixtures, as a result of application to the property's historical or acquisition cost. Valuation factors are intended to be applied directly to the historical/acquisition cost of the equipment and/or fixture, in order to estimate its value. Thus, valuation factors reflect both price changes and loss of value (depreciation) over time, in a single factor. The valuation factors presented are by year of acquisition.

NOTE: while all the demonstrations, examples, and exercises shown in this lesson use lien date 2011 for illustrative purposes, it must be remembered that it is the lien date for which values are sought that determines which AH 581 – and associated factors – will be used. The Board of Equalization's website contains several years of AH 581 publications, which can be accessed through: AH 581 Tables.

Definitions

This lesson uses several terms that you should be familiar with; below are definitions for certain terms that are used throughout this lesson.

- Business Property Statement: property statements are declarations of assessable property signed under penalty of perjury. They report all taxable property owned, claimed, possessed, controlled, or managed by the person filing it. They are prescribed forms upon which California taxpayers report their assessable business property to county assessors. (Assessable is synonymous with taxable.)

- Market Value: price (the amount of money) that a property would bring if exposed for sale in the open market under conditions in which neither buyer nor seller could take advantage of the exigencies of the other, and both the buyer and seller have knowledge of all the uses and purposes to which the property is adapted and for which it is capable of being used. It is also referred to as fair market value. (Refer to definition in Lesson 1 for additional information.)

Non-Production Computers

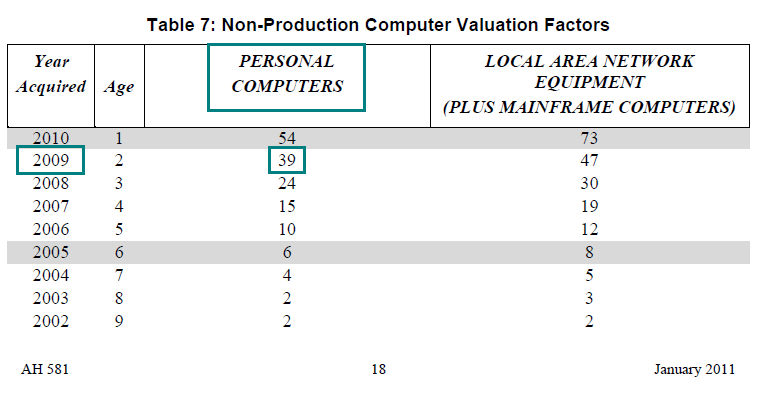

The first of the five valuation factor tables provided in AH 581 is for non-production computer equipment. Non-production computers are defined as general purpose computers and peripherals, and local area network (LAN) devices; not including telecommunication equipment or lines used to connect LAN's, and computer equipment embedded in machinery or specifically designed for use in applications directly related to manufacturing. A more detailed description of what “non-production computers” consist of is provided in Chapter 3 of AH 581.

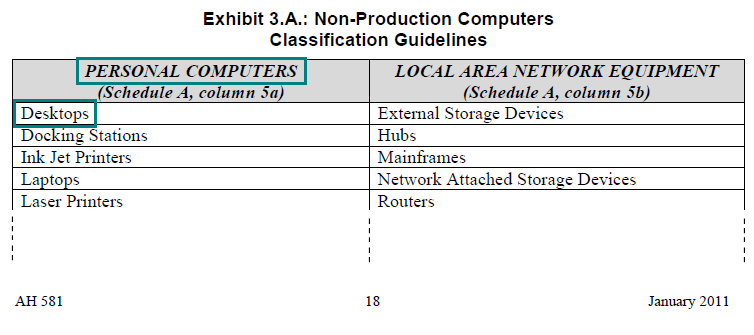

Table 7, Non-Production Computer Valuation Factors, was derived as the result of a BOE conducted Valuation Factor Study – an analysis of market data. This valuation factor table is divided into two groups of equipment: (1) personal computers; and, (2) local area network equipment; local area network equipment includes mainframe computers. AH 581 includes a list to serve as guidance in the classification of non-production computers into the two aforementioned groups. Note: these two groups of equipment correspond to reporting schedules on the Business Property Statement form used by California county assessors for taxpayer reporting. Exhibit 3.A. in AH 581 identifies the specific area (schedule and column) of the form upon which taxpayers are to report costs – Schedule A, column 5a for personal computers and Schedule A-1, column 5b for local area network equipment.

Application of the value factors found in Table 7 of AH 581, to the acquisition (historical) cost of non-production computer equipment is rebuttably presumed to produce the market value of such equipment; this is specified by Revenue and Taxation Code section 401.20. As indicated in Table 7, county assessors or taxpayers may provide evidence to overcome this presumption.

Demonstration of Use of Non-Production Computers Valuation Factors

The following is a step-by-step demonstration of how to use the Non-Production Computer Valuation Factors, found in AH 581 Table 7, to estimate the market value of non-production computer system equipment based on the acquisition cost and year of the equipment:

- Ascertain the type of equipment being valued(personal computers or local area network equipment) and its acquisition cost and year. (Refer to the classification guidelines list provided in Exhibit 3.A. Non-Production Computers Classification Guidelines on pages 18 of AH 581 to ascertain the appropriate type of non-production computer equipment.)

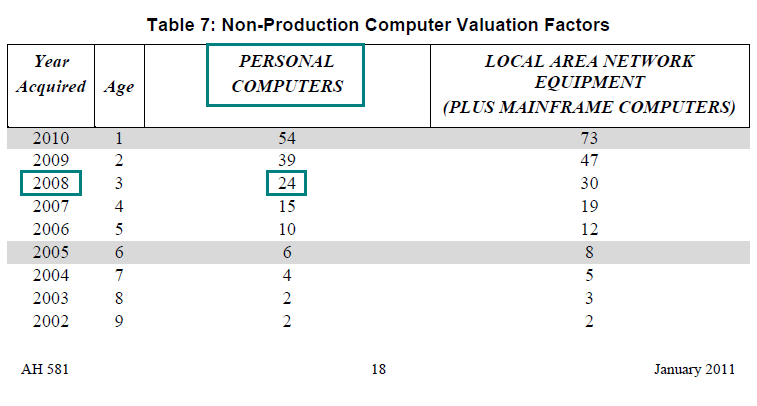

In 2008, a business acquired and installed desktop computers (personal computers) at a cost of $10,000. (According to the Classification Guidelines, desktops are personal computers.)

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of equipment value is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the valuation factor corresponding to the equipment's year of acquisition and type (personal computers or local area network equipment plus mainframe computers) using Table 7: Non-Production Computer Valuation Factors, of the previously selected AH 581 (2011). (As indicated in step 1, AH 581 provides classification guidelines to determine the type of computer equipment. Those guidelines in Exhibit 3.A. on page 18 list desktop computers as personal computers.)

2008 Year Acquired & Personal Computers = 24

(Note: According to the classification guidelines shown in step 1 – the “Personal Computers” valuation factors are the appropriate factors for use in valuing desktop computers.)

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step. $10,000 × 0.24 = $2,400 Thus, by applying the applicable valuation factor to the acquisition cost of the personal computers, it is estimated that this equipment, purchased in 2008 for $10,000, has a market value of $2,400, as of lien date 2011 (January 1, 2011).

Practical Applications of Non-Production Computers Valuation Factors

The following examples are designed to illustrate how to estimate the market value of non-production computer equipment using the Non-Production Computer Equipment Valuation Factors found in Table 7 of AH 581:

Example 1:

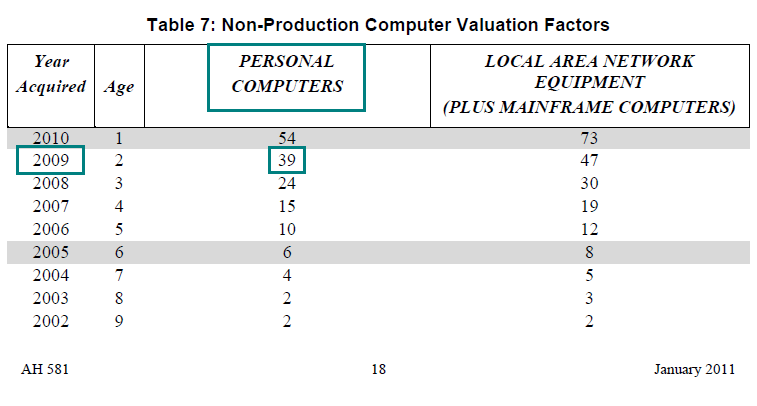

What is the market value (full cash value), as of lien date 2011 (January 1), of 50 laptop computers purchased by a business in 2009, for $100,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $100,000 × 0.39

- Market Value = $39,000

- Locate the valuation factor for personal computers with a 2009 acquisition year in Table 7: Non-Production Computer Valuation Factors of the January 2011 AH 581. (Note: a laptop computer is classified in the “personal computers” category in accordance with the non-production computers classification guidelines outlined in Exhibit 3.A. of AH 581.) 2009 Year Acquired & Personal Computers = 39

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$100,000 × 0.39 = $39,000

Example 2:

What is the market value (full cash value), as of lien date 2011 (January 1), of a laser printer purchased and installed in 2009, for $40,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $40,000 × 0.39

- Market Value = $15,600

- Locate the valuation factor for personal computers with a 2009 acquisition year, in Table 7: Non-Production Computer Valuation Factors of the January 2011 AH 581. (Note: a laser printer is classified in the “personal computers” category in accordance with the non-production computers classification guidelines outlined in Exhibit 3.A., page 18, of AH 581.) 2009 Year Acquired & Personal Computers = 39

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$40,000 × 0.39 = $15,600

Example 3:

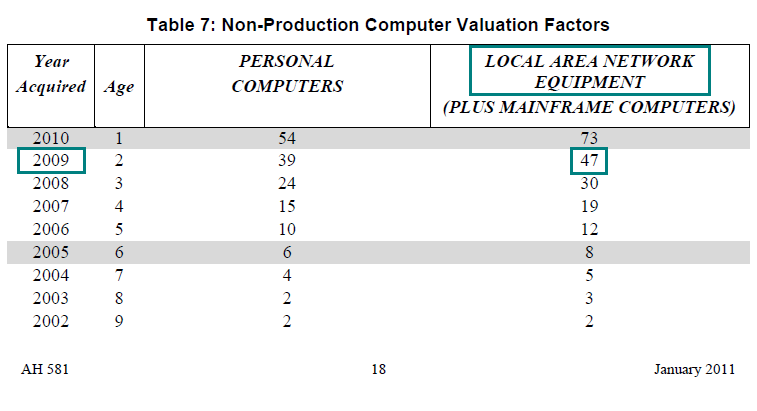

What is the market value (full cash value), as of lien date 2011 (January 1), of a mainframe computer server purchased and installed in 2009, for $100,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $100,000 × 0.47

- Market Value = $47,000

- Locate the valuation factor for local area network equipment plus mainframe computers with a 2009 acquisition year, in Table 7: Non-Production Computer Valuation Factors of the January 2011 AH 581. (Note: a mainframe server is classified in the “local area network equipment plus mainframe computers” category in accordance with the non-production computers classification guidelines outlined in Exhibit 3.A. of AH 581.) 2009 Year Acquired & Local Area Network Equipment Plus Mainframe Computers = 47

- Calculate the market value of the equipment, as of the lien date (January 1, 2010), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$100,000 × 0.47 = $47,000

Semiconductor Manufacturing Equipment & Fixtures

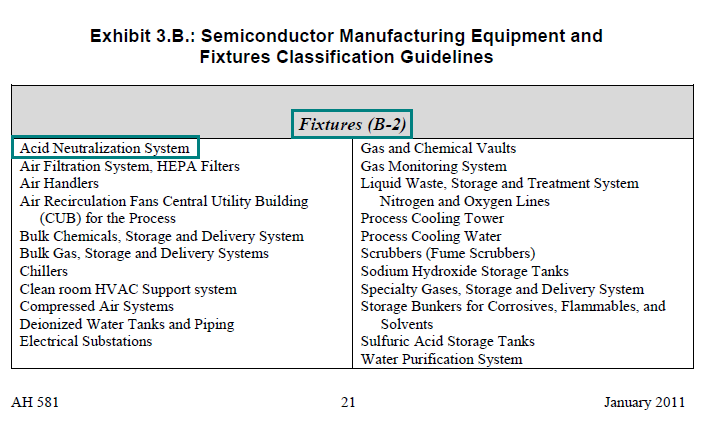

The second of the five valuation factor tables provided in AH 581 is for semiconductor manufacturing equipment and fixtures. In general, the following semiconductor manufacturing equipment and fixtures qualify for application of the Table 8 valuation factors: (1) clean room manufacturing equipment used for the fabrication of semiconductor chips; (2) test equipment used in manufacturing, research & development, and semiconductor manufacturing equipment testing; and (3) fixtures in place to support a semiconductor fabrication facility. A more detailed definition of “semiconductor manufacturing equipment and fixtures” is provided in Chapter 3 of AH 581.

Table 8, Semiconductor Manufacturing Equipment and Fixtures Valuation Factors, was derived as the result of a BOE conducted Valuation Factor Study – an analysis of market data. This valuation factor table is divided into two groups of equipment: (1) machinery and equipment; and, (2) fixtures. AH 581 includes a list to serve as guidance in the classification of semiconductor manufacturing equipment and fixtures into the two aforementioned groups. Note: these two groups of equipment correspond to reporting schedules on the Business Property Statement form used by California county assessors for taxpayer reporting of assessable property. The table identifies the specific area of the form upon which taxpayers are to report costs – Schedule A-1 for the equipment and Schedule B-2 for fixtures.

The semiconductor manufacturing machinery and equipment valuation factors are based on an untrended 6-year economic life (a 6-year average service (economic) life not indexed for price changes). The valuation factors for semiconductor manufacturing fixtures are based on a trended 10-year economic life (a 10-year average service (economic) life indexed for price changes).

Application of the value factors found in Table 8 of AH 581, to the acquisition (historical) cost of semiconductor manufacturing equipment and fixtures is rebuttably presumed to produce the market value of such equipment and fixtures; this is specified by Revenue and Taxation Code section 401.20.

Note: An 8% minimum percent good factor was employed in the derivation of the Table 8 Semiconductor Manufacturing Machinery and Equipment Valuation Factors. A 10% minimum percent good factor was employed in the derivation of the Table 8 Semiconductor Manufacturing Fixtures Valuation Factors.

Demonstration of Use of Semiconductor Manufacturing Equipment & Fixtures Valuation Factors

The following is a step-by-step demonstration of how to use the Semiconductor Manufacturing Equipment and Fixtures Valuation Factors, found in AH 581 Table 8, to estimate the market value of semiconductor manufacturing equipment and fixtures based on the acquisition cost and year of the equipment or fixture:

- Ascertain the classification of property being valued (equipment or fixture) and its acquisition cost and year. (Refer to the classification guidelines list provided in Exhibit 3.B. Semiconductor Manufacturing Equipment and Fixtures Classification Guidelines on pages 20 and 21 of AH 581 to ascertain the appropriate class for the property.)

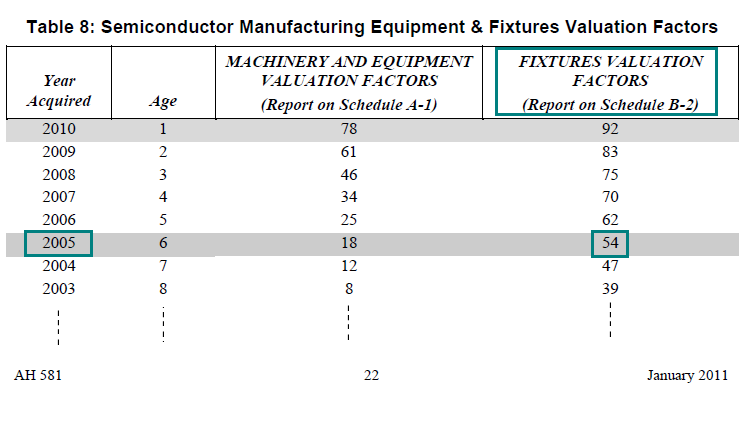

In 2005, a semiconductor fabrication plant acquired and installed an acid neutralization system at a cost of $500,000. (According to the Classification Guidelines, an acid neutralization system is classified as a fixture.)

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of equipment or fixture value is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the valuation factor corresponding to the property's year of acquisition and class (equipment or fixture) using the 2011 AH 581 Table 8: Semiconductor Manufacturing Equipment and Fixtures Valuation Factors of the previously selected AH 581 (2011). (As indicated in step 1, AH 581 provides classification guidelines to determine the appropriate classification for the property. Those guidelines in Exhibit 3.B., on page 21, list acid neutralization system as a fixture.)

2005 Year Acquired & Fixtures = 54

(Note: According to the classification guidelines shown in step 1 – the “Personal Computers” valuation factors are the appropriate factors for use in valuing desktop computers.)

- Calculate the market value of the fixture, as of the lien date (January 1, 2011), by multiplying the fixture's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step. $500,000 × 0.54 = $270,000 Thus, by applying the applicable valuation factor to the acquisition cost of the acid neutralization system, it is estimated that this fixture, purchased in 2005 for $500,000, has a market value of $270,000, as of lien date 2011 (January 1, 2011).

Practical Applications of Semiconductor Manufacturing Equipment & Fixtures Valuation Factors

The following examples are designed to illustrate how to estimate the market value of semiconductor manufacturing equipment and fixtures using the Semiconductor Manufacturing Equipment and Fixtures Valuation Factors, found in Table 8 of AH 581:

Example 1:

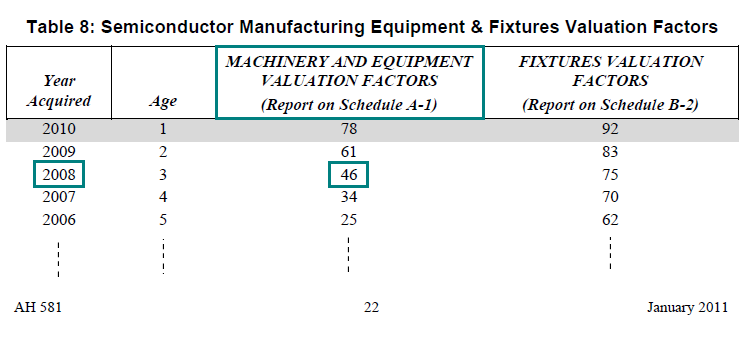

What is the market value, as of lien date 2011 (January 1), of a plasma etcher purchased and installed by a semiconductor manufacturer in 2008, for $150,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $150,000 × 0.46

- Market Value = $69,000

- Locate the valuation factor for semiconductor machinery and equipment with a 2008 acquisition year in Table 8: Semiconductor Manufacturing Equipment and Fixtures Valuation Factors of the January 2011 AH 581. (Note: a plasma etcher is classified in the “machinery and equipment” category in accordance with the semiconductor classification guidelines outlined in Exhibit 3.B., page 20, of AH 581.) 2008 Year Acquired & Machinery and Equipment = 46

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$150,000 × 0.46 = $69,000

Example 2:

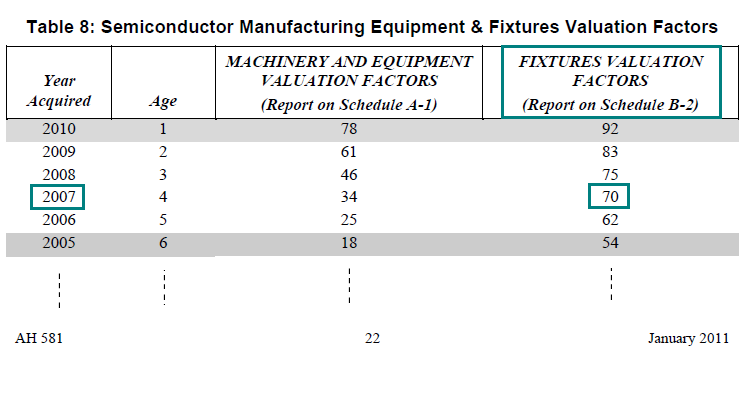

What is the market value, as of lien date 2011 (January 1), of gas monitoring system purchased and installed by a semiconductor manufacturer in 2007, for $500,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $500,000 × 0.70

- Market Value = $350,000

- Locate the valuation factor for semiconductor fixtures with a 2007 acquisition year in Table 8: Semiconductor Manufacturing Equipment and Fixtures Valuation Factors of the January 2011 AH 581. (Note: a gas monitoring system is classified in the “fixtures” category in accordance with the semiconductor classification guidelines outlined in Exhibit 3.B., page 21, of AH 581.) 2007 Year Acquired & Fixtures = 70

- Calculate the market value of the fixture, as of the lien date (January 1, 2011), by multiplying the fixture's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$500,000 × 0.70 = $350,000

Example 3:

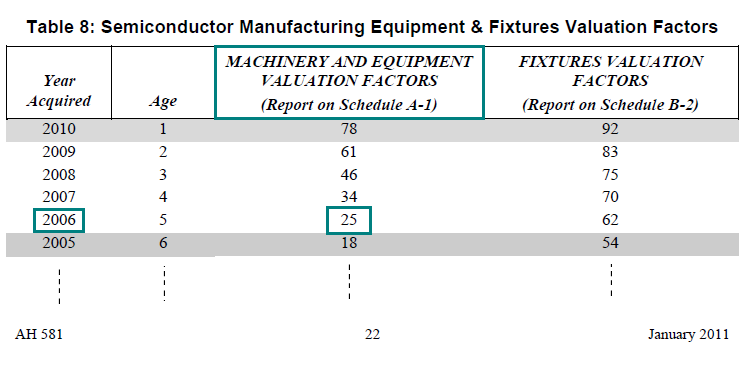

What is the market value, as of lien date 2011 (January 1), of a laser annealer purchased and installed by a semiconductor manufacturer in 2006, for $250,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $250,000 × 0.25

- Market Value = $62,500

- Locate the valuation factor for semiconductor fixtures with a 2006 acquisition year in Table 8: Semiconductor Manufacturing Equipment and Fixtures Valuation Factors of the January 2011 AH 581. (Note: a laser annealer is classified in the "machinery and equipment" category in accordance with the semiconductor classification guidelines outlined in Exhibit 3.B., pages 20 and 21, of AH 581.) 2006 Year Acquired & Machinery and Equipment = 25

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$250,000 × 0.25 = $62,500

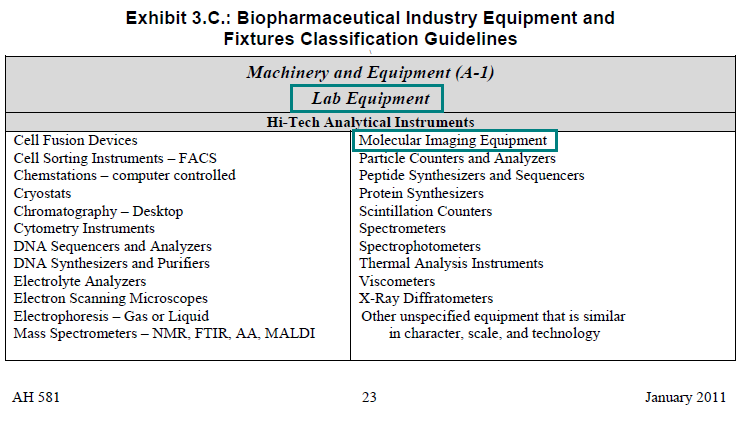

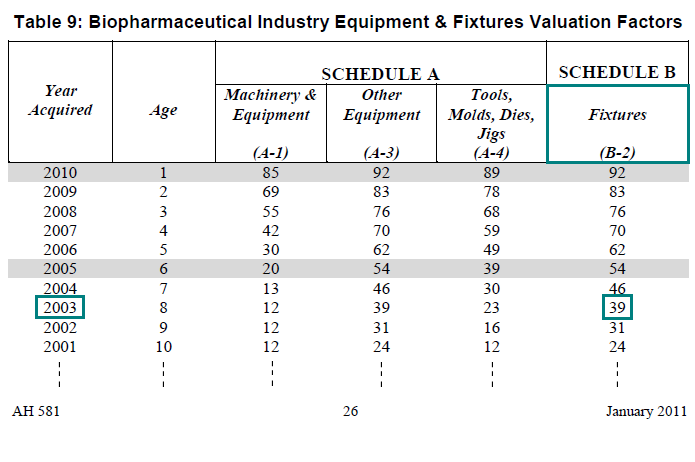

Biopharmaceutical Industry Equipment & Fixtures

The third of the five valuation factor tables provided in AH 581 is for biopharmaceutical industry equipment and fixtures. In general, the following biopharmaceutical industry equipment and fixtures qualify for application of the Table 9 valuation factors: equipment and fixtures utilized in connection with, or in support of, research and/or manufacturing activities that use organisms, or materials derived from organisms, their cellular, subcellular, or molecular components, to discover and/or provide products for human or animal therapeutics, diagnostics, and/or vaccines. Other equipment and/or fixtures — such as office equipment or computer equipment — should be valued as such using applicable index, percent good, or valuation factor tables in the AH 581. A more detailed definition of “biopharmaceutical industry equipment and fixtures” is provided in Chapter 3 of AH 581.

Table 9, Biopharmaceutical Industry Equipment and Fixtures Valuation Factors, was derived as the result of a BOE conducted Valuation Factor Study — an analysis of market data. This valuation factor table is divided into four groups of equipment: (1) machinery and equipment; (2) other equipment; (3) tools, molds, dies, jigs; and, (4) fixtures. AH 581 includes a list to serve as guidance in the classification of biopharmaceutical industry equipment and fixtures into the four aforementioned groups. The table identifies “Schedule A” for the three equipment types and “Schedule B” for fixtures; this corresponds to the property statement reporting form used by California county assessors for taxpayer reporting of assessable property.

Application of the value factors found in Table 9 of AH 581, to the acquisition (historical) cost of biopharmaceutical industry equipment and fixtures is rebuttably presumed to produce the market value of such equipment and fixtures; this is specified by Revenue and Taxation Code section 401.20.

Note: If a minimum value factor is employed in conjunction with the use of Table 9 value factors, its use must be determined in a supportable manner.

Demonstration of Use of Biopharmaceutical Industry Equipment & Fixtures Valuation Factors

The following is a step-by-step demonstration of how to use the Biopharmaceutical Industry Equipment and Fixtures Valuation Factors, found in AH 581 Table 9, to estimate the market value of biopharmaceutical industry equipment and fixtures based on the acquisition cost and year of the equipment or fixture:

- Ascertain the classification of property being valued (equipment or fixture), the type of equipment for property classified as equipment, and its acquisition cost and year. (Refer to the classification guidelines list provided in Exhibit 3.C: Biopharmaceutical Industry Equipment and Fixtures Classification Guidelines, on page 23 through 25, of AH 581 to ascertain the appropriate class for the property and appropriate category within the equipment class.)

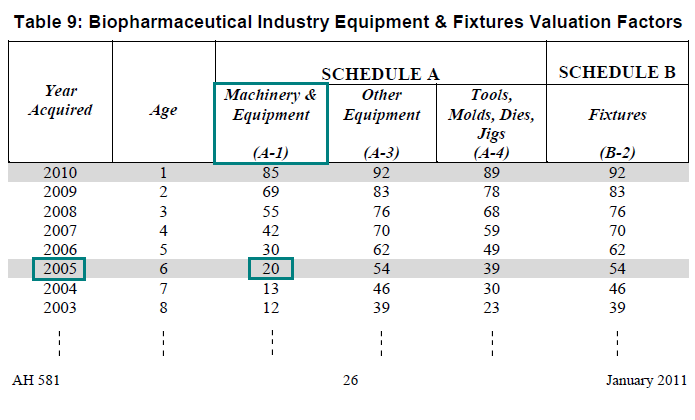

In 2005, a biopharmaceutical company acquired and installed desktop molecular imaging equipment at a cost of $800,000. (According to the Classification Guidelines, molecular imaging equipment is classified as a fixture and categorized as lab equipment.)

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of equipment or fixture value is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the valuation factor corresponding to the property's year of acquisition, class (equipment or fixture), and, if equipment, equipment type (lab equipment, commercial manufacturing equipment, or pilot scale manufacturing equipment) using the 2011 AH 581 Table 9: Biopharmaceutical Industry Equipment and Fixtures Valuation Factors of the previously selected AH 581. (As indicated in step 1 above, AH 581 provides classification guidelines to determine the appropriate class and type. Those guidelines in Exhibit 3.C. on page 23 list molecular imaging equipment as lab equipment.)

2005 Year Acquired & Lab Equipment (Machinery & Equipment [A-1]) = 20

(Note: According to the classification guidelines shown in step 1 – the “Machinery & Equipment (A-1)” valuation factors are the appropriate factors for use in valuing molecular imaging equipment.)

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step. $800,000 × 0.20 = $160,000 Thus, by applying the applicable valuation factor to the acquisition cost of the molecular imaging equipment, it is estimated that this equipment, purchased in 2005 for $800,000, has a market value of $160,000, as of lien date 2011 (January 1, 2011).

Practical Applications of Biopharmaceutical Industry Equipment & Fixtures Valuation Factors

The following examples are designed to illustrate how to estimate the market value of biopharmaceutical industry equipment and fixtures using the Biopharmaceutical Industry Equipment and Fixtures Valuation Factors, found in Table 9 of AH 581:

Example 1:

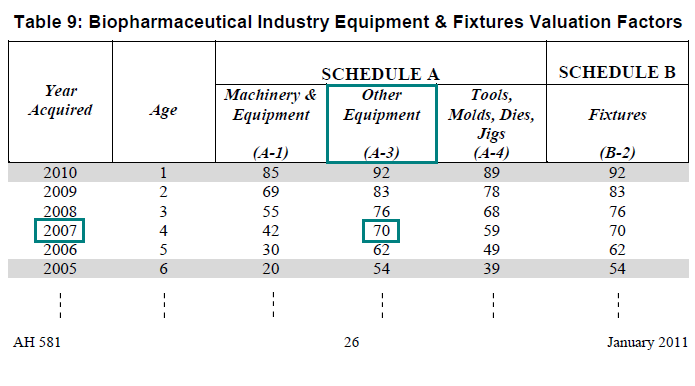

What is the market value, as of lien date 2011 (January 1), of a clean room monitor purchased and installed by a biopharmaceutical company in 2007, for $350,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $350,000 × 0.70

- Market Value = $245,000

- Locate the valuation factor for biopharmaceutical industry "other equipment" with a 2007 acquisition year in Table 9, Biopharmaceutical Industry Equipment and Fixtures Valuation Factors of the January 2011 AH 581. (Note: a clean room monitor is classified in the equipment category under "other equipment — commercial manufacturing equipment" in accordance with the biopharmaceutical industry classification guidelines outlined in Exhibit 3.C., page 24, of AH 581.) 2007 Year Acquired & Other Equipment (A-3) = 70

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$350,000 × 0.70 = $245,000

Example 2:

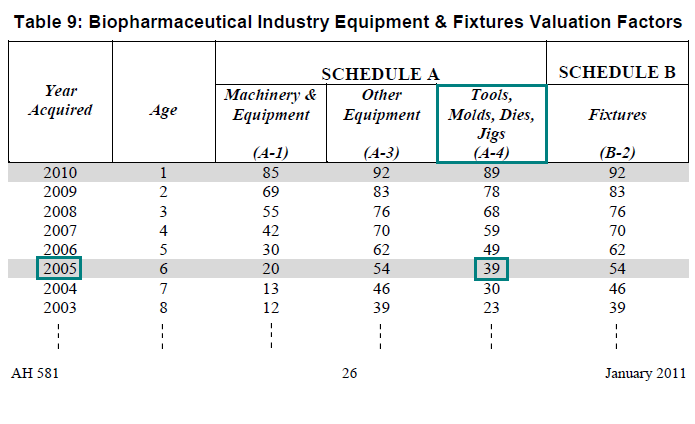

What is the market value, as of lien date 2011 (January 1), of a pilot scale mixer purchased and installed by a biopharmaceutical company in 2005, for $125,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $125,000 × 0.39

- Market Value = $48,750

- Locate the valuation factor for biopharmaceutical industry “tools, molds, dies, jigs” with a 2005 acquisition year in Table 9: Biopharmaceutical Industry Equipment and Fixtures Valuation Factors of the January 2011 AH 581. (Note: a pilot scale mixer is classified in the equipment category under “tools, molds, dies, jigs” in accordance with the biopharmaceutical industry classification guidelines outlined in Exhibit 3.C., page 25 of AH 581.) 2005 Year Acquired & Pilot Scale Manufacturing Equipment (A-4) = 39

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$125,000 × 0.39 = $48,750

Example 3:

What is the market value, as of lien date 2011 (January 1), of a walk-in freezer purchased and installed by a biopharmaceutical company in 2003, for $85,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $85,000 × 0.39

- Market Value = $33,150

- Locate the valuation factor for biopharmaceutical industry “fixtures” with a 2003 acquisition year in Table 9: Biopharmaceutical Industry Equipment and Fixtures Valuation Factors of the January 2011 AH 581. (Note: a walk-in-freezer is classified in the equipment category under “fixtures and process piping” in accordance with the biopharmaceutical industry classification guidelines outlined in Exhibit 3.C., page 25 of AH 581.) 2003 Year Acquired & Fixtures = 39

- Calculate the market value of the fixture, as of the lien date (January 1, 2011), by multiplying the fixture's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$85,000 × 0.39 = $33,150

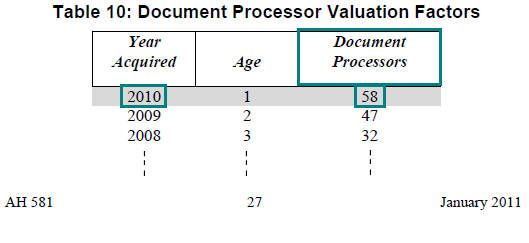

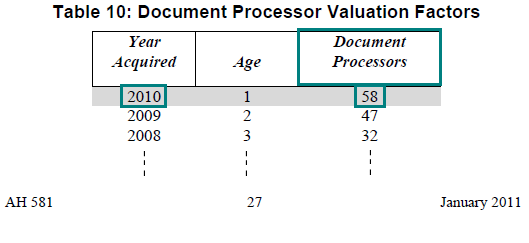

Document Processors

The fourth of the five valuation factor tables provided in AH 581 is for document processors. Document processors are defined as: analog “light-lens” devices, as well as digital devices, which contain a document scanning system and a print controller; including both stand-alone copiers, and multifunction printers (MFP) capable of copying, scanning, printing, and faxing. A more detailed definition of “document processor” is provided in Chapter 3 of AH 581.

Table 10, Document Processor Valuation Factors, was derived as the result of a BOE conducted Valuation Factor Study — an analysis of market data.

Application of the value factors found in Table 10 of AH 581, to the acquisition (historical) cost of document processors is intended to estimate the market value of such equipment.

Note: Table 10 valuation factors reflect a 10% minimum value factor for devices beyond the age of eight (8) years.

Demonstration of Use of Document Processors Valuation Factors

The following is a step-by-step demonstration of how to use the Document Processor Valuation Factors, found in AH 581 Table 10, to estimate the market value of document processors based on the acquisition cost and year of the equipment:

- Ascertain the acquisition cost and year of the equipment. In 2010, a business acquired a copier at a cost of $10,000.

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of equipment value is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the valuation factor corresponding to the equipment's year of acquisition, using Table 10: Document Processor Valuation Factors of the previously selected AH 581 (2011).

2010 Year Acquired = 58

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the value factor (percent) found in the preceding step. $10,000 × 0.58 = $5,800 Thus, by applying the applicable valuation factor to the acquisition cost of the copier, it is estimated that this equipment, purchased in 2010 for $10,000, has a market value of $5,800, as of lien date 2011 (January 1, 2011).

Practical Applications of Document Processors Valuation Factors

The following examples are designed to illustrate how to estimate the market value of document processors using the Document Processor Valuation Factors, found in Table 10 of AH 581:

Example 1:

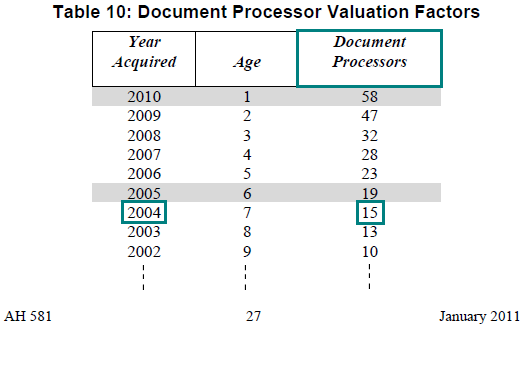

What is the market value, as of lien date 2011 (January 1), of a high speed copier purchased and installed by a business in 2004, for $25,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $25,000 × 0.15

- Market Value = $3,750

- Locate the valuation factor for document processors with a 2004 acquisition year in Table 10: Document Processor Valuation Factors of the January 2011 AH 581. 2004 Year Acquired = 15

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$25,000 × 0.15 = $3,750

Example 2:

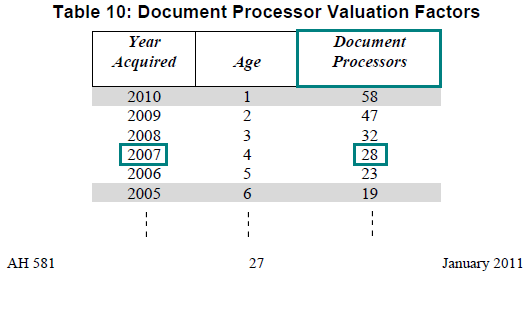

What is the market value, as of lien date 2011 (January 1), of a multifunction printer (printing, scanning, coping, and faxing) purchased and installed by a business in 2007, for $10,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $10,000 × 0.28

- Market Value = $2,800

- Locate the valuation factor for document processors with a 2007 acquisition year in Table 10: Document Processor Valuation Factors of the January 2011 AH 581. 2007 Year Acquired = 28

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$10,000 × 0.28 = $2,800

Example 3:

What is the market value, as of lien date 2011 (January 1), of a copier purchased by a business in 2010, for $23,500?

Solution:

- Market Value = Cost x Valuation Factor (converted to a decimal equivalent)

- Market Value = $23,500 × 0.58

- Market Value = $13,630

- Locate the valuation factor for document processors with a 2010 acquisition year in Table 10: Document Processor Valuation Factors of the January 2011 AH 581. 2010 Year Acquired = 58

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$23,500 × 0.58 = $13,630

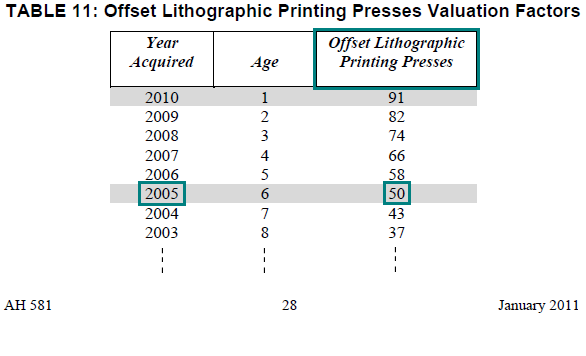

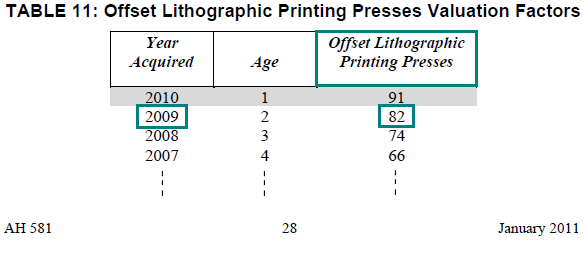

Offset Lithographic Printing Presses

The fifth of the five valuation factor tables provided in AH 581 is for offset lithographic printing presses. The offset lithographic printing press valuation factors are intended for use in the valuation of sheet fed offset lithography printing presses. They are not intended for use in the valuation of plateless or non-impact (digital or quick printing) printing presses or web fed (continuous feed) printing presses. They are also not intended for use in the valuation of other equipment used in print production, such as: “prepress” equipment – equipment used to transform an original into a state that is ready for reproduction – and “postpress” equipment – equipment used to finish or bind the printed material. A more detailed definition of “offset lithographic printing press” is provided in Chapter 3 of AH 581.

Table 11, Offset Lithographic Printing Presses Valuation Factors, was derived as the result of a BOE conducted Valuation Factor Study – an analysis of market data.

Application of the value factors found in Table 11 of AH 581, to the acquisition (historical) cost of offset lithographic printing presses is intended to estimate the market value of such equipment.

Note: A 10% minimum value factor is employed in the Table for devices beyond the age of 13 years.

Demonstration of Use of Offset Lithographic Printing Presses Valuation Factors

The following is a step-by-step demonstration of how to use the Offset Lithographic Printing Presses Valuation Factors, found in AH 581 Table 11, to estimate the market value of offset lithographic printing presses based on the acquisition cost and year of the equipment:

- Ascertain the acquisition cost and year of the equipment. In 2005, a printing company acquired a sheet feed offset lithography printing press at a cost of $100,000.

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of equipment value is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the valuation factor for offset lithographic printing press equipment with a 2005 acquisition year in Table 11: Offset Lithographic Printing Presses Valuation Factors of the previously selected AH 581 (2011).

2005 Year Acquired = 50

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the value factor (percent) found in the preceding step. $100,000 × 0.50 = $50,000 Thus, by applying the applicable valuation factor to the acquisition cost of the sheet feed offset lithographic printing press, it is estimated that this equipment, purchased in 2005 for $100,000, has a market value of $50,000, as of lien date 2011 (January 1, 2011).

Practical Applications of Offset Lithographic Printing Presses Valuation Factors

The following examples are designed to illustrate how to estimate the market value of offset lithographic printing presses, using the Offset Lithographic Printing Presses Valuation Factors, found in Table 11 of AH 581:

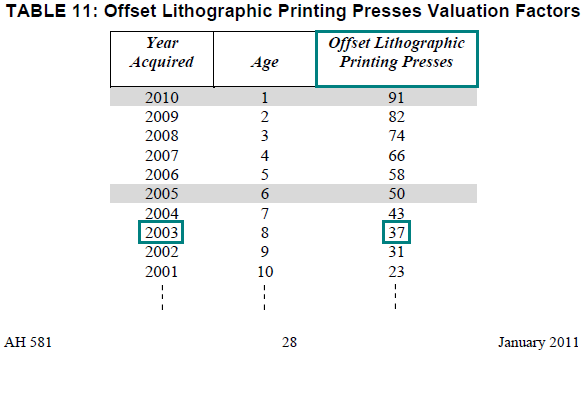

Example 1:

What is the market value, as of lien date 2011 (January 1), of an ACME 9150 2-color sheet feed offset lithographic printing press purchased and installed by a printing business in 2003, for $10,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $10,000 × 0.37

- Market Value = $3,700

- Locate the valuation factor for offset lithographic printing press equipment with a 2003 acquisition year in Table 11: Offset Lithographic Printing Presses Valuation Factors of the January 2011 AH 581. 2003 Year Acquired = 37

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$10,000 × 0.37 = $3,700

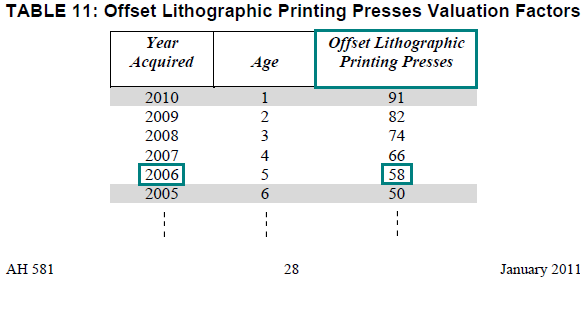

Example 2:

What is the market value, as of lien date 2011 (January 1), of a PowerPress 16 4-color sheet feed offset lithographic printing press purchased and installed by a printing business in 2006, for $65,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $65,000 × 0.58

- Market Value = $37,700

- Locate the valuation factor for offset lithographic printing press equipment with a 2006 acquisition year in Table 11: Offset Lithographic Printing Presses Valuation Factors of the January 2011 AH 581. 2006 Year Acquired = 58

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$65,000 × 0.58 = $37,700

Example 3:

What is the market value, as of lien date 2011 (January 1), of a PrintMaster 590 4-color sheet feed offset lithographic printing press purchased and installed by a printing business in 2009, for $70,000?

Solution:

- Market Value = Cost × Valuation Factor (converted to a decimal equivalent)

- Market Value = $70,000 × 0.82

- Market Value = $57,400

- Locate the valuation factor for offset lithographic printing press equipment with a 2009 acquisition year in Table 11: Offset Lithographic Printing Presses Valuation Factors of the January 2011 AH 581. 2009 Year Acquired = 82

- Calculate the market value of the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the valuation factor (percent) found in the preceding step.

$70,000 × 0.82 = $57,400

Lesson Summary

The lesson you just read on application of valuation factors demonstrates how to arrive at estimates of market value for certain specific categories of equipment and fixtures using the valuation factors for such specific categories of equipment and fixtures published in the AH 581.

In some cases, selection of the applicable valuation factor is based on only the acquisition year and category of equipment being valued; i.e., equipment subject to valuation via Table 10: Document Processors and Table 11: Offset Lithographic Printing Presses.

In other cases, selection of the applicable valuation factor is based on the type of equipment or classification of the property – personal property versus fixture – within a category, as well as the acquisition year and category of the equipment or fixture being valued; i.e., equipment or fixtures subject to valuation via Table 7: Non-Production Computers, Table 8: Semiconductor Manufacturing Equipment and Fixtures, and Table 9: Biopharmaceutical Industry Equipment and Fixtures.

Note: Before proceeding on to the next lesson, be sure to complete the exercises for this lesson.