Lesson 2 – Index Factors (Valuation of Personal Property and Fixtures)

Using Assessors' Handbook Section 581 (Equipment Index, Percent Good, and Valuation Factors)

Appraisal Training: Self-Paced Online Learning Session

This lesson discusses index factors, one of the three types of factor tables – index, percent good, and valuation – that are published annually by the Board in Assessors' Handbook Section 581 (AH 581), Equipment and Fixtures Index, Percent Good and Valuation Factors. AH 581 index factors are used for estimating the reproduction cost new (RCN) of equipment and fixtures, on the basis of such property's cost and year of acquisition. Index factors are presented in the following three AH 581 tables:

- Table 1: Commercial Equipment

- Table 2: Industrial Equipment

- Table 3: Agricultural and Construction Equipment

The index factors published in AH 581 are based on indexes published annually by the U.S. Bureau of Labor Statistics and equipment price data published annually by Marshall & Swift/-Boeckh, LLC.

Application of the index factors published in AH 581 to the original cost of property typically approximates reproduction cost new, since the information on which the factors are based tracks price level changes over time.

In the case where the equipment or fixtures have experienced rapid changes in technology, the reproduction cost new of such property will likely require adjustment – to eliminate the effects of functional obsolescence – in order to equate reproduction cost new to replacement cost new. In other words, due to changes in technology it may now cost less to produce suitable replacement equipment or fixtures than would be the case if such equipment or fixtures were still being produced using technologies and materials present when they were acquired.

Assessors' Handbook Section 581 recommends the use of a maximum index factor to address the effect of rapid technological change experienced by equipment or fixtures; where such adjustment of the otherwise applicable index factor is appropriate. Use of a recommended maximum index factor is briefly discussed below and further explained in Lesson 6: Factor Adjustments.

NOTE: while all the demonstrations, examples, and exercises shown in this lesson use lien date 2011 for illustrative purposes, it must be remembered that it is the lien date for which values are sought that determines which AH 581 – and associated factors – will be used. The Board of Equalization's website contains several years of AH 581 publications; they can be accessed through AH 581 Tables

After reading the lesson, check your knowledge by completing the exercises at the end of the lesson.

Open All Close AllDefinitions

- Reproduction Cost New: The cost of replacing an existing property with an identical property – an exact duplicate – as of a particular date. (Note: Where the equipment or fixtures have undergone minimal changes in technology, the reproduction cost new of such property is likely to be similar to its replacement cost new – replacement cost new being the desired basis for estimating a property's market value.)

- Replacement Cost New: The cost of replacing an existing property with a property of equivalent utility – a substitute property – as of a particular date.

- Functional Obsolescence is the loss in value caused by the design of the property itself. A decline in the capacity of the property to perform the function for which it was intended; due to such things as: changes in technologies and manufacturing processes; changes in marketplace tastes; changes in equipment design, materials, or process; or, poor initial equipment design.

- Equipment: the term “equipment” should be thought to encompass fixtures, as well, when used by itself in discussions relative to the applicability of index and/or percent good factors to the valuation of such. (Fixtures are discussed in Lesson 1: Overview.)

Commercial Equipment

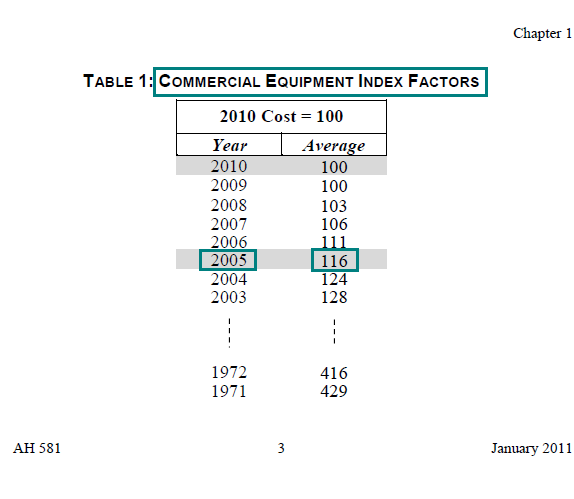

One of the three index factor tables presented in AH 581 is for commercial equipment. The factors for commercial equipment are provided in Table 1. The factors published in Table 1 are intended for use in estimating the market value of commercial equipment. The factors are presented according to year of acquisition.

Application of the index factors found in Table 1, of AH 581, to the original cost of equipment, typically produces the reproduction cost new (RCN) for such equipment. Percent good factors are then applied to RCN to arrive at an estimate of market value for the equipment. Application of percent good factors is discussed in Lesson 3: Percent Good Factors. A discussion of cost, including historical and original, and valid cost components can be found in Lesson 7: Cost and Cost Components.

Table 1, Commercial Equipment Index Factors, was compiled based on equipment price data published annually by the Marshall & Swift/Boeckh, LLC, Marshall Valuation Service. Eleven classes of commercial equipment index factors were averaged to produce the Table 1 index factors:

- Bank, Garage, Hospital, Hotel, Laundry, Library, Office, Restaurant, Retail, Theater, and Warehouse.

Due to rapid technological changes which have taken place in recent years, it is recommended that a maximum index factor be used when valuing commercial equipment.

- The recommended maximum index factor is that factor corresponding to equipment of an age equal to 125% of the estimated average service life (economic life) of such equipment.

- See Lesson 6: Factor Adjustments for an example on how to calculate and use this recommended maximum index factor. Additionally, average service life is discussed in Lesson 5: Determining the Economic Life / Average Service Life of Equipment and Fixtures.

Demonstration of Using Commercial Equipment Index Factors to Calculate RCN

The following is a step-by-step demonstration of how to use the Commercial Equipment Index Factors, found in AH 581 Table 1, to estimate the reproduction cost new (RCN) of commercial equipment based on the equipment's acquisition cost and year.

- Ascertain the type of equipment and its acquisition cost and year. In 2005, a business acquired office equipment at a cost of $10,000.

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of the equipment's reproduction cost new is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the index factor corresponding to the year the equipment was acquired, using Table 1, Commercial Equipment Index Factors, of the previously selected AH 581 (2011).

2005 Year Acquired = 116

- Calculate the reproduction cost new (RCN) for the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step. RCN = $10,000 × 1.16 = $11,600 Thus, it is estimated that it would cost approximately $11,600, on lien date 2011 (January 1, 2011), to purchase office equipment identical to that purchased in 2005 for $10,000. In other words, office equipment identical to that purchased in 2005 for $10,000, would cost $11,600 if purchased on January 1, 2011.

Practical Applications of Using Commercial Equipment Index Factors to Calculate RCN

The following examples are designed to illustrate how to estimate the reproduction cost new (RCN) of commercial equipment using the Commercial Equipment Index Factors found in Table 1 of AH 581. While all the examples shown below use lien date 2011 for illustrative purposes, it must be remembered that it is the lien date for which values are sought that determines which AH 581 – and associated factors – will be used.

Note: for purposes of these examples only, disregard application of the Recommended Maximum Index Factor, it will be covered in a separate lesson – Lesson 6: Factor Adjustments.

Example 1:

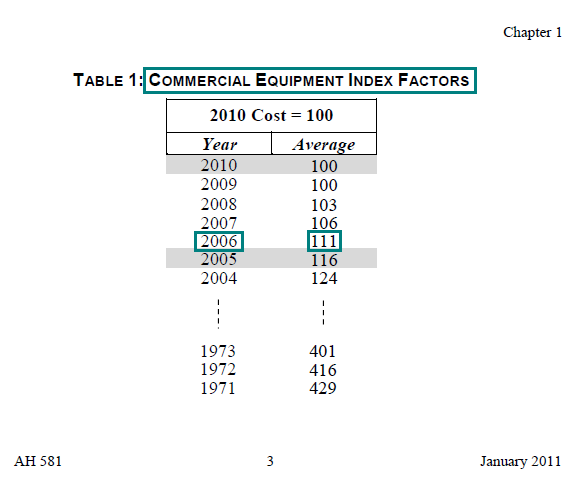

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for restaurant equipment purchased and installed in 2006, for $50,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $50,000 × 1.11

- RCN = $55,500

- Locate the index factor for commercial equipment with a 2006 acquisition year, in Table 1 of the January 2011 AH 581. 2006 Year Acquired = 111

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $50,000 × 1.11 = $55,500

Example 2:

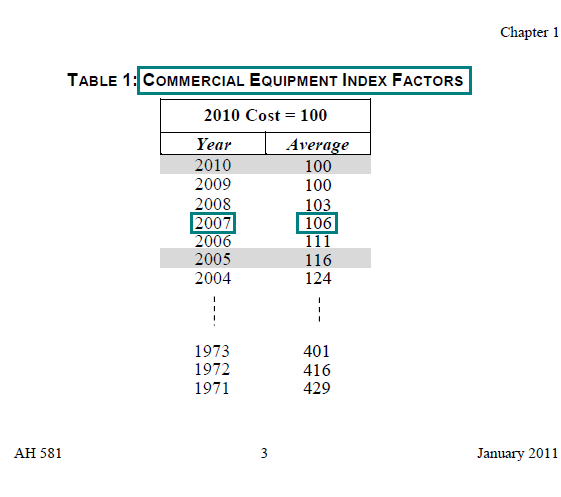

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for grocery store equipment purchased and installed in 2007, for $50,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $50,000 × 1.06

- RCN = $53,000

- Locate the index factor for commercial equipment with a 2007 acquisition year, in Table 1 of the January 2011 AH 581. 2007 Year Acquired = 106

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $50,000 × 1.06 = $53,000

Industrial Equipment

The second index factor table presented in AH 581 is for industrial equipment; the factors are provided in Table 2. The factors published in Table 2, are intended for use in estimating the market value of industrial equipment. The factors are presented according to year of acquisition.

Application of the index factors found in Table 2, of AH 581, to the historical or original cost of equipment, typically produces the reproduction cost new (RCN) of such equipment. Percent good factors are then applied to RCN to arrive at an estimate of market value for the equipment. Application of percent good factors is discussed in Lesson 3: Percent Good Factors. A discussion of cost, including historical and original, and valid cost components can be found in Lesson 7: Cost and Cost Components.

Table 2, Industrial Machinery and Equipment Index Factors, was derived using the Bureau of Labor Statistics' Producer Price Indexes as a basis. The factors for twenty-seven Industry Classes were averaged to produce the Table 2 index factors:

- Aerospace; Cement Manufacturing; Chemicals and Allied Products; Electrical Equipment Manufacturing; Electronic Equipment; Fabricated Metal Products; Food and Kindred Products; Glass and Glass Products; Grain and Grain Mill Products; Leather and Leather Products; Lumber, Wood Products, and Furniture; Machinery (except Electrical, Metal Working, and Transportation); Mining; Motor Vehicles and Parts; Paper Finishing; Petroleum Exploration and Production; Petroleum Refining; Plastics Products; Primary Metals; Professional and Scientific Instruments; Printing and Publishing; Pulp and Paper; Rubber Products; Stone and Clay Products (except Cement); Sugar and Sugar Products; Textile Mill Products; and Vegetable Oil Products.

- For a listing of each of these classes with a detailed description of each industry class, see AH 581, Exhibit 1A.

{kind=link}

NOTE: Use of a single category of factors for industrial equipment provides value estimates within a reasonable band of value for the assessment of business property using mass appraisal techniques. For purposes of reporting costs on the business property statement filed with county assessors, costs are reported in aggregate by type of equipment and year of acquisition; individual pieces of equipment are not detailed.

Due to rapid technological changes which have taken place in recent years, it is recommended that a maximum index factor be used when valuing industrial equipment.

- The recommended maximum index factor is that factor corresponding to equipment of an age equal to 125% of the estimated average service life (economic life) of such equipment.

- See Lesson 6: Factor Adjustments for an example on how to calculate and use this recommended maximum index factor. Additionally, average service life is discussed in Lesson 5: Determining the Economic Life / Average Service Life of Equipment and Fixtures.

Demonstration of Using Industrial Equipment Index Factors to Calculate RCN

The following is a step-by-step demonstration of how to use the Industrial Machinery and Equipment Index Factors, found in AH 581 Table 2, to estimate the reproduction cost new (RCN) of industrial equipment based on the equipment's acquisition cost and year:

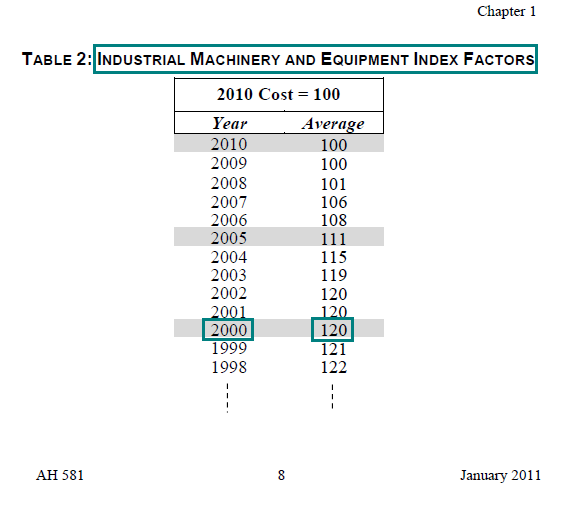

- Ascertain the type of equipment and its acquisition cost and year. In 2000, a cement manufacturer acquired cement manufacturing equipment at a cost of $1,000,000.

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of the equipment's reproduction cost new is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the index factor corresponding to the year the equipment was acquired, using Table 2, Industrial Equipment Index Factors, of the previously selected AH 581 (2011).

2000 Year Acquired = 120

- Calculate the reproduction cost new (RCN) for the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step. RCN = $1,000,000 × 1.20 = $1,200,000 Thus, it is estimated that it would cost approximately $1,200,000, on lien date 2011 (January 1, 2011), to purchase cement manufacturing equipment identical to that purchased in 2000 for $1,000,000. In other words, cement manufacturing equipment identical to that purchased in 2000 for $1,000,000, would cost $1,200,000, if purchased on January 1, 2011.

Practical Applications of Using Industrial Equipment Index Factors to Calculate RCN

The following examples are designed to illustrate how to estimate the reproduction cost new (RCN) of industrial equipment using the Industrial Machinery and Equipment Index Factors found in Table 2 of AH 581. While all the examples shown below use lien date 2011 for illustrative purposes, it must be remembered that it is the lien date for which values are sought that determines which AH 581 – and associated factors – will be used.

Note: for purposes of these examples only, disregard application of the Recommended Maximum Index Factor to make adjustment for technological changes in calculating replacement cost new, it will be covered in a separate lesson – Lesson 6: Factor Adjustments.

Example 1:

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for food processing equipment purchased and installed in 2000, for $500,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $500,000 × 1.20

- RCN = $600,000

- Locate the index factor for industrial equipment with a 2000 acquisition year, in Table 2 of the January 2011 AH 581. 2000 Year Acquired = 120

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $500,000 × 1.20 = $600,000

Example 2:

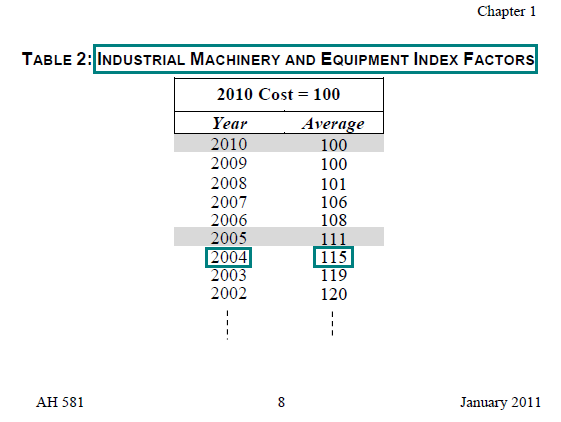

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for apparel (clothing) manufacturing equipment purchased and installed in 2004, for $250,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $250,000 × 1.15

- RCN = $287,500

- Locate the index factor for industrial equipment with a 2004 acquisition year, in Table 2 of the January 2011 AH 581. 2004 Year Acquired = 115

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $250,000 × 1.15 = $287,500

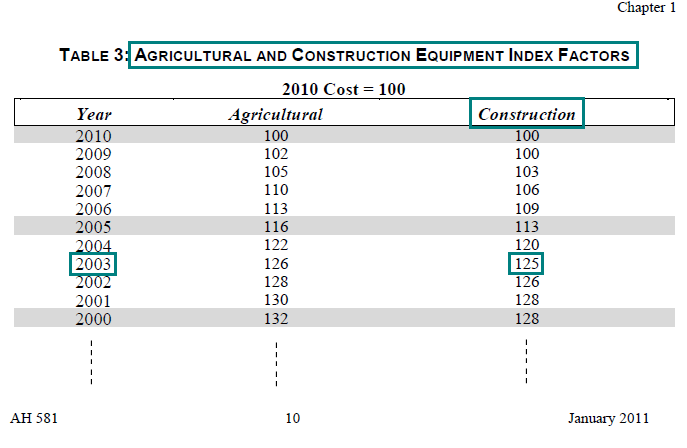

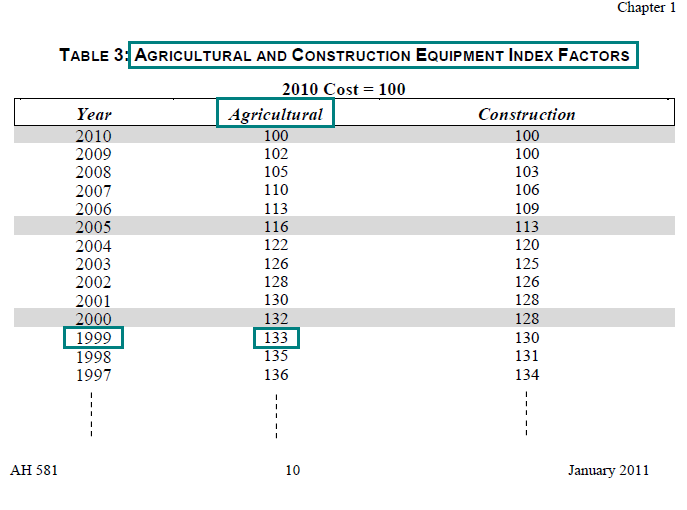

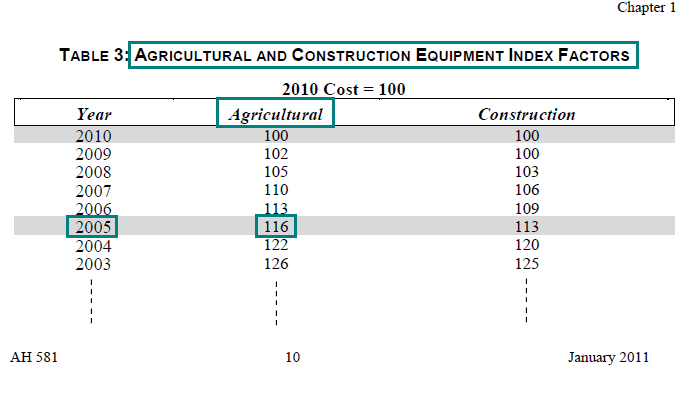

Construction Equipment

The third index factor table presented in AH 581 contains factors for both agricultural equipment and construction equipment; both sets of factors are provided in Table 3. The factors published in Table 3, are intended for use in estimating the market value of agricultural equipment or construction equipment. The index factors for both types of equipment are presented according to year of acquisition.

The factors found in Table 3, are also intended for use regardless of whether or not such equipment is mobile or non-mobile. The reason for the distinction will be more apparent in Lesson 3 where the use of percent good factors to convert reproduction cost new (RCN) into reproduction cost new less (normal) depreciation (RCNLD), or market value, is discussed. While non-mobile construction and agricultural equipment both use Table 3, index factors, to calculate RCN, and Table 4, percent good factors, to calculate RCNLD, mobile construction and agricultural equipment both use separate percent good factor tables to calculate RCLND. Mobile construction equipment uses Table 5, percent good factors, to calculate the RCLND for mobile construction equipment; and, mobile agricultural equipment uses Table 6, percent good factors, to calculate RCLND for mobile agricultural equipment.

Table 3, Agricultural and Construction Equipment Index Factors, was derived using the Bureau of Labor Statistics' Producer Price Indexes as a basis.

Due to rapid technological changes which have taken place in recent years, it is recommended that a maximum index factor be used when valuing construction equipment.

- The recommended maximum index factor is that factor corresponding to equipment of an age equal to 125% of the estimated average service life (economic life) of such equipment.

- See Lesson 6: Factor Adjustments for an example on how to calculate and use this recommended maximum index factor. Additionally, average service life is discussed in Lesson 5: Determining the Economic Life / Average Service Life of Equipment and Fixtures.

Demonstration of Using Construction Equipment Index Factors to Calculate RCN

The following is a step-by-step demonstration of how to use the Construction Equipment Index Factors, found in AH 581 Table 3, to estimate the reproduction cost new (RCN) of construction equipment (mobile and non-mobile) based on the equipment's acquisition cost and year:

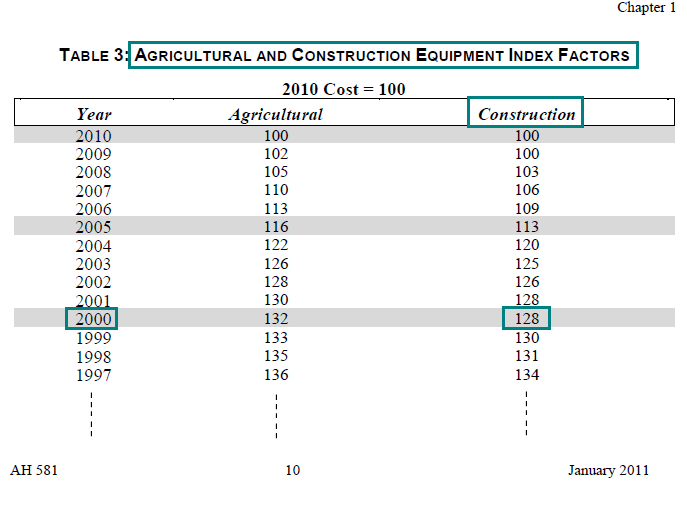

- Ascertain the type of equipment and its acquisition cost and year. In 2000, a construction firm acquired a used motor grader (mobile construction equipment) and a light plant (non-mobile construction equipment), at a cost of $100,000 each.

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of the equipment's reproduction cost new is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the index factor (construction) corresponding to the year the equipment was acquired, using Table 3, Agricultural and Construction Equipment Index Factors, of the previously selected AH 581 (2011).

2000 Year Acquired = 128

- Calculate the reproduction cost new (RCN) for the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step. RCN (motor grader) = $100,000 × 1.28 = $128,000 RCN (light plant) = $100,000 × 1.28 = $128,000 Total RCN = $200,000 × 1.28 = $256,000 Thus, it is estimated that it would cost approximately $256,000 on lien date 2011 (January 1, 2011), to purchase a motor grader and light plant identical to that purchased in 2000 for $200,000 ($100,000 each). In other words, a motor grader and light plant identical to that purchased in 2000 for $200,000, would cost $256,000, if purchased on January 1, 2011.

Practical Applications of Using Construction Equipment Index Factors to Calculate RCN

The following examples are designed to illustrate how to estimate the reproduction cost new (RCN) of construction equipment using the Construction Equipment Index Factors found in Table 3 of AH 581. While all the examples shown below use lien date 2011 for illustrative purposes, it must be remembered that it is the lien date for which values are sought that determines which AH 581 – and associated factors – will be used.

Note: for purposes of these examples only, disregard application of the Recommended Maximum Index Factor, it will be covered in a separate lesson – Lesson 6: Factor Adjustments.

Example 1 (non-mobile construction equipment):

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for a large volume pump (non-mobile construction equipment) purchased and installed in 2003, for $50,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $50,000 × 1.25

- RCN = $62,500

- Locate the index factor for construction equipment with a 2003 acquisition year, in Table 3 of the January 2011 AH 581. 2003 Year Acquired = 125

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $50,000 × 1.25 = $62,500

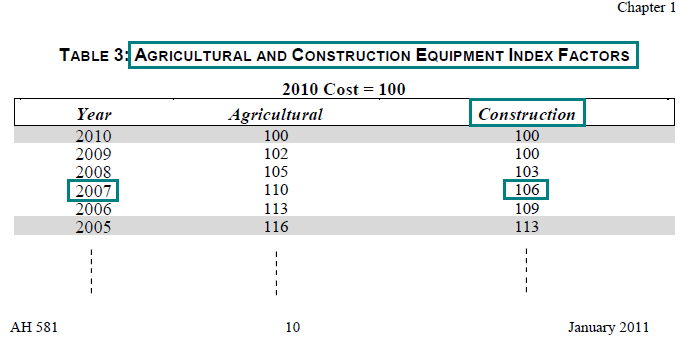

Example 2 (mobile construction equipment):

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for a bulldozer purchased used and delivered in 2007, for $120,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $120,000 × 1.06

- RCN = $127,200

- Locate the index factor for construction equipment with a 2007 acquisition year, in Table 3 of the January 2011 AH 581. 2007 Year Acquired = 106

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $120,000 × 1.06 = $127,200

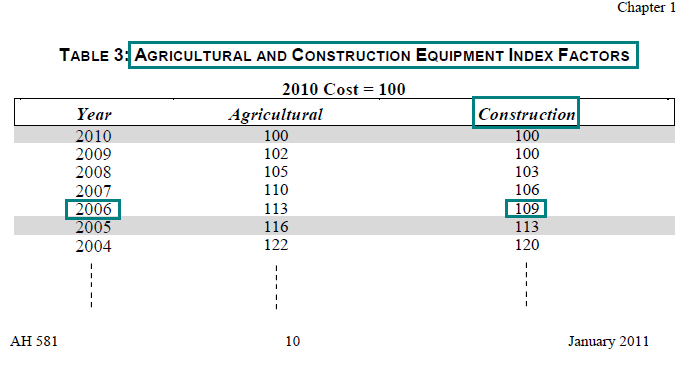

Example 3 (mobile construction equipment):

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for a truck-mounted crane purchased new and delivered in 2006, for $120,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $120,000 × 1.09

- RCN = $130,800

- Locate the index factor for construction equipment with a 2006 acquisition year, in Table 3 of the January 2011 AH 581. 2006 Year Acquired = 109

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $120,000 × 1.09 = $130,800

Agricultural Equipment

As previously indicated under the discussion on construction equipment, the third index factor table presented in AH 581 contains factors for both agricultural equipment and construction equipment; both sets of factors are provided in Table 3. The factors published in Table 3, are intended for use in estimating the market value of agricultural equipment or construction equipment. Both sets of factors are presented according to year of acquisition.

Application of the index factors found in Table 3, of AH 581, to the historical or original cost of equipment, typically produces the reproduction cost new for such equipment.

Similar to the index factors for construction equipment in Table 3, Agricultural and Construction Equipment Index Factors, the agricultural index factors were derived using the Bureau of Labor Statistics' Producer Price Indexes as a basis.

Due to rapid technological changes which have taken place in recent years, it is recommended that a maximum index factor be used when valuing agricultural equipment.

- The recommended maximum index factor is that factor corresponding to an age equal to 125% of the estimated average service life (economic life) of such equipment.

- See Lesson 6: Factor Adjustments for an example on how to calculate and use this recommended maximum index factor. Additionally, average service life is discussed in Lesson 5: Determining the Economic Life / Average Service Life of Equipment and Fixtures.

Demonstration of Using Agricultural Equipment Index Factors to Calculate RCN

The following is a step-by-step demonstration of how to use the Agricultural Equipment Index Factors, found in AH 581 Table 3, to estimate the reproduction cost new (RCN) of agricultural equipment (mobile and non-mobile) based on the equipment's acquisition cost and year:

- Ascertain the type of equipment and its acquisition cost and year. In 2004, a farm acquired a new cotton harvester (mobile agricultural equipment) and a cotton gin (non-mobile agricultural equipment), at a cost of $100,000 each.

- Select the appropriate AH 581 (published annually) based on the lien date (January 1, XXXX) for which the estimate of the equipment's reproduction cost new is sought.

January 2011 AH 581 (lien date 2011 chosen for illustrative purposes only)

- Locate the index factor (agricultural) corresponding to the year the equipment was acquired, using Table 3, Agricultural and Construction Equipment Index Factors, of the previously selected AH 581 (2011).

2004 Year Acquired = 122

- Calculate the reproduction cost new (RCN) for the equipment, as of the lien date (January 1, 2011), by multiplying the equipment's acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step. RCN (cotton harvester) = $100,000 × 1.22 = $122,000 RCN (cotton gin) = $100,000 × 1.22 = $122,000 Total RCN = $200,000 × 1.22 = $244,000 Thus, it is estimated that it would cost approximately $244,000 on lien date 2011 (January 1, 2011), to purchase a cotton harvester and cotton gin identical to that purchased in 2004 for $200,000 ($100,000 each). In other words, a cotton harvester and cotton gin identical to that purchased in 2004 for $200,000, would cost $244,000, if purchased on January 1, 2011.

Practical Applications of Using Agricultural Equipment Index Factors to Calculate RCN

The following examples are designed to illustrate how to estimate the reproduction cost new (RCN) of agricultural equipment using the Agricultural Equipment Index Factors found in Table 3 of AH 581. While all the examples shown below use lien date 2011 for illustrative purposes, it must be remembered that it is the lien date for which values are sought that determines which AH 581 – and associated factors – will be used.

Note: for purposes of these examples only, disregard application of the Recommended Maximum Index Factor, it will be covered in a separate lesson – Lesson 6: Factor Adjustments.

Example 1 (non-mobile agricultural equipment):

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for dairy equipment (non-mobile agricultural equipment) purchased and installed in 1999, for $150,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $150,000 × 1.33

- RCN = $199,500

- Locate the index factor for agricultural equipment with a 1999 acquisition year, in Table 3 of the January 2011 AH 581. 1999 Year Acquired = 133

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $150,000 × 1.33 = $199,500

Example 2 (mobile agricultural equipment):

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for a farm tractor purchased new and delivered in 2005, for $150,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $150,000 × 1.16

- RCN = $174,000

- Locate the index factor for agricultural equipment with a 2005 acquisition year, in Table 3 of the January 2011 AH 581. 2005 Year Acquired = 116

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $150,000 × 1.16 = $174,000

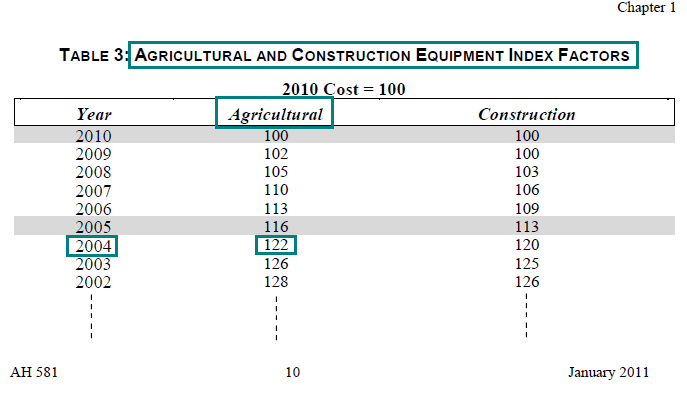

Example 3 (mobile agricultural equipment):

What is the reproduction cost new (RCN), as of lien date 2011 (January 1), for a rice combine purchased used and delivered in 2004, for $150,000?

Solution:

- RCN = Cost × Index Factor (converted to decimal equivalent)

- RCN = $150,000 × 1.22

- RCN = $183,000

- Locate the index factor for agricultural equipment with a 2004 acquisition year, in Table 3 of the January 2011 AH 581. 2004 Year Acquired = 122

- Calculate the reproduction cost new (RCN) for the equipment, by multiplying its acquisition cost by the decimal equivalent of the index factor (percent) found in the preceding step.

RCN = $150,000 × 1.22 = $183,000

Lesson Summary

The lesson you just read on application of index factors demonstrates how to arrive at estimates of reproduction cost new of equipment using the factors published in the AH 581. Reproduction cost new is used to arrive at market value estimates of equipment through application of percent good factors. Application of percent good factors is discussed in Lesson 3: Percent Good Factors.

Note: Before proceeding on to the next lesson, be sure to complete the exercises for this lesson.