Lesson 7: Periodic Repayment

Check Your Knowledge

In order to solve the following problems you will need to refer to AH 505 to look up the factors in the compound interest tables. Before you start, please print the problems using the "Print Questions" button below so you can work through the problems on your own. After you work through the problem, the solution can be viewed by clicking on the blue plus sign immediately following the question. Additionally, when you have completed all the problems, you may print all of the solutions using the "Print Questions with Answers" button below.

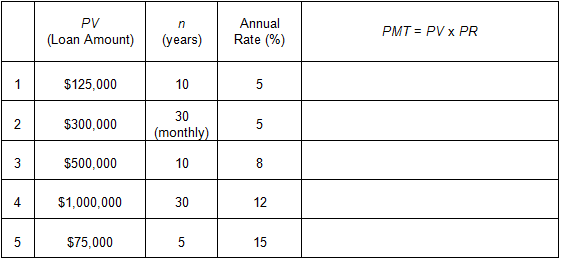

Problem 1

Calculate the payment amount (PMT) for each loan amount using the Periodic Repayment (PR) factors in AH 505:

Solution

Solution:

To solve, calculate the payment amount by multiplying the loan amount by the PR factor found in the AH 505 compound interests tables for the given interest rate and term.

PMT = PV × PR

PMT = $125,000 × 0.129505 (AH 505, page 29, column 6)

PMT = $16,188.13

PMT = PV × PR

PMT = $300,000 × 0.005368 (AH 505, page 28, column 6)

PMT = $1,610.40

PMT = PV × PR

PMT = $500,000 × 0.149029 (AH 505, page 41, column 6)

PMT = $74,514.50

PMT = PV × PR

PMT = $1,000,000 × 0.124144 (AH 505, page 57, column 6)

PMT = $124,144.00

PMT = PV × PR

PMT = $75,000 × 0.298316 (AH 505, page 69, column 6)

PMT = $22,373.70

Problem 2

You take out a car loan for $8,000 at an annual interest rate of 10% with 48 monthly payments due at the end of each month. What is the monthly payment?

Solution

Solution:

To solve, calculate the payment amount using the monthly PR factors in the annual compound interest tables of AH 505.

Multiply the loan amount by the PR factor for the interest rate of 10% (monthly) for a 4 year term.

PMT = PV × PR (10%, 4 yrs, monthly)

PMT = $8,000 × 0.025363 (AH 505, page 48, column 6)

PMT = $202.90

The monthly payment is $202.90.

Problem 3

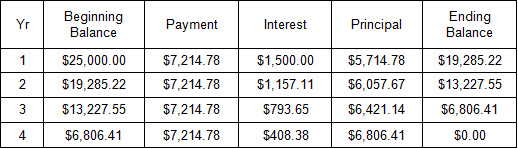

Show the amortization schedule for a loan of $25,000 at an annual rate of 6% that will be repaid in four annual end-of-period installments.

Solution

Solution:

The interest payment for each year is equal to the beginning loan balance (outstanding principal) multiplied by the annual rate (for year 1, $25,000.00 × 0.06 = $1,500.00).

The principal repayment for each year is equal to the difference between the payment amount and the interest amount (for year 1, $7,214.78 - $1,500.00 = $5,714.78).

The principal payment for each year reduces the beginning loan balance for the following year (beginning balance year 2, $25,000.00 - $5,714.78 = $19,285.22).

Problem 4

Joan will deposit $4,000 at the end of each year for 15 years, after which she will withdraw the balance in 20 equal annual installments, beginning at the end of year 16. Assuming an annual interest rate of 12% throughout, how much can she withdraw each year?

Solution

Solution:

This exercise combines the use of the Future Worth of $1 Per Period (FW$1/P) and the PR factors.

First, calculate the future amount at the end of year 15 using the FW$1/P factor.

Second, calculate the payment amount that will amortize this future amount over the ensuing 20 years using the PR factor. That´s how much Joan can withdraw each year for the next 20 years with nothing left over.

Calculate the future value by multiplying the deposit amount by the FW$1/P factor for the interest rate of 12% and a 15 year term.

FV = PMT × FW$1/P (12%, 15 yrs, annual)

FV = $4,000 × 37.279715 (AH 505, page 57, column 2)

FV = $149,119.86

Calculate the payment that will amortize the above future value by multiplying the future value by the PR factor for the interest rate of 12% for a 20 year term.

PMT = PV × PR (12%, 20 yrs, annual)

PMT = $149,119 × 0.133879 (AH 505, page 57, column 6)

PMT = $19,963.63